If you watch Fox News or listen to any conservative pundits, you will hear about Reagan on an almost daily basis, usually in reference to his economic success. Generally, the liberal pundit response is very underwhelming. At worst, you get some mention of deficits (which were of course high under Reagan) and at best you get some sort of non-sequitur about his foreign policy (which was of course aggressive and criminal). Neither of these points — or any of the others often raised — strike at the heart of the Reagan myth. In reality, Reagan had little to do with the economy’s upswing in the 1980s: the economy’s improvement was almost entirely a function of monetary policy over which he had no control.

It is understandable why this is rarely mentioned. Few understand monetary policy, especially among the pundit class. Fiscal and tax policy is simple enough, but when you start getting into the domain of the monetary base, interest rates, and inflation, heads start to spin. However, you will not understand the economy under Reagan without understanding what the Federal Reserve was doing. It was the Fed that drove the economic swings in the late 1970s throughout the 1980s, not Reagan’s fiscal or tax policies.

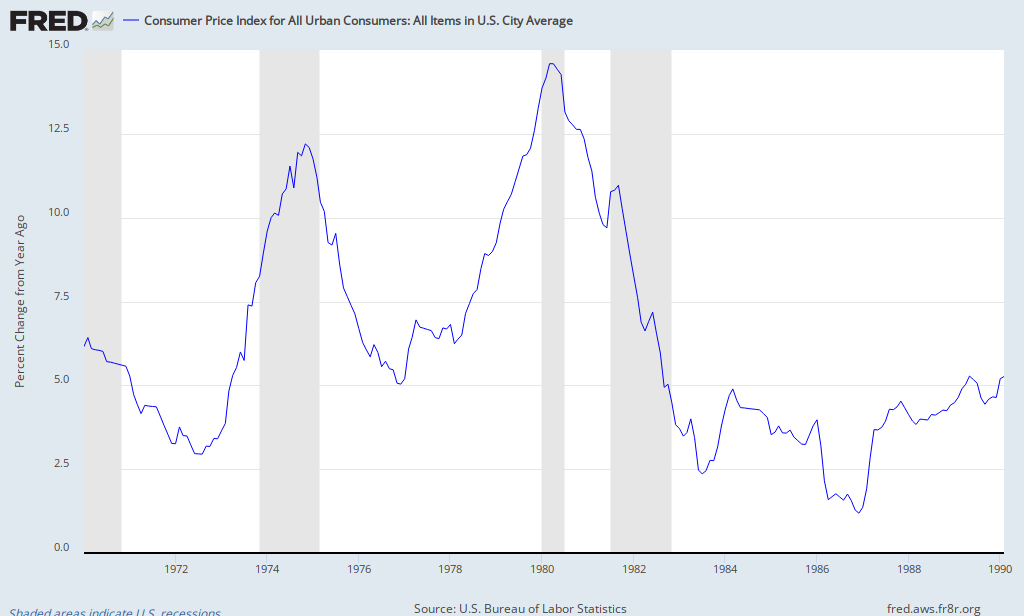

In the 1970s, inflation soared. In December of 1976, inflation was at 5 percent, meaning that the prices of goods and services were rising at a rate of 5 percent each year. From that low point, inflation steadily rose until it reached a high of 14.6 percent in March and April of 1980. By comparison, the modern Fed targets an inflation rate of 2 percent.

{kind=link}

To combat this inflation, the Federal Reserve increased interest rates. The interest rate hikes were extreme, and the federal funds rate reached as high as 19.1 percent in June of 1980. By comparison, the federal funds rate is currently near 0 and only went above 5 percent a few times in the last decade. Hiking interest rates slows economic activity, and the intent of the Fed was to create an economic recession that would whip inflation. This policy accomplished exactly that as the rate hikes caused (or dominantly contributed to) the 1980 recession and the recession that spanned 1981-1982.

{kind=link}

After the Fed was convinced it had beaten inflation back, it rapidly cut interest rates to bring the economy back to capacity and full employment. So starting in August of 1981, the Fed began its rate cuts. From the 19.1 percent interest rate high in June of 1980, the rates fell as low as 2.4 percent in July of 1983 and all the way to 1.2 percent in December of 1986. Cutting rates like this stimulates the economy (if it is not already operating at capacity) and that’s exactly what it did.

In this time period of rate hikes and rate cuts, the unemployment rate bounced up and then down in tune with Fed policy (with some lag time which is typical). After hovering around 5-6 percent for most of the late 1970s, the unemployment rate shot up. In July of 1979, the unemployment rate was at 5.7 percent. The rate rose and rose until it finally reached its peak in December of 1982 at 10.8 percent. Then, responding to the steep interest rate cuts described above, the rate plummeted almost entirely uninterrupted until it settled back around 5-6 percent. The low point was 5.3 percent in November and December of 1988.

{kind=link}

So, in short, the Federal Reserve sought to tackle extremely high inflation rates that presented themselves in the late 1970s. It did this by hiking interest rates to slow down economic activity and create a recession. After it had accomplished that, it cut the interest rates to bring the economy back to capacity. This rate hike and subsequent rate cut caused unemployment to spike and then fall, after the usual lag.

Reagan managed to come into the office right as the rate hikes were icing the economy and throwing people out of work, and then managed to remain in office as the rate cuts were bringing the economy back to capacity and full employment. But Reagan had nothing to do with any of this. The Fed chair that engineered this, Paul Volcker, was not even appointed by Reagan: Carter appointed him. However, since nobody understands monetary policy, this is all missed, and instead we get treated to a totally ignorant discussion about Reagan’s fiscal and tax policy as if they were even remotely important drivers of these economic swings.

To be clear, none of what I have said here is original or unique. In economic circles, this is the most generic and standard explanation of what was going on. The Federal Reserve is almost always the most important actor in reducing or increasing unemployment. In a world where everyone on TV and radio has no real idea what the Federal Reserve does, this fact gets buried. But if you want to understand what happened in the late 1970s and 1980s, you wont even start to comprehend it without looking at the monetary policy of that period.